One in eight American adults is now taking a GLP-1 drug. That number has more than doubled in eighteen months.

That is not a trend.

That is a structural shift.

And if you make, market, or sell snack food, the data from Cornell, Numerator, and Circana tell a story you cannot ignore.

The people on these medications are not just eating differently. They are buying differently.

And the categories they are walking away from first are the ones that have driven snack-aisle growth over the past two decades.

Who Is Using GLP-1 Drugs and How Fast Is This Growing?

The headline number comes from RAND Corporation research published in August 2025: 11.8 percent of U.S. adults have used a GLP-1 such as Ozempic or Wegovy.

A separate Gallup survey from mid-to-late 2025 put the weight-loss-specific number at 12.4 percent, up from 5.8 percent in February 2024. Prescriptions have more than tripled since 2020.

The household picture is even more striking. Circana reports that 23 percent of U.S. households now have at least one GLP-1 user. By 2030, they project that GLP-1 households will represent 35 percent of all food and beverage units sold in this country.

Who is on these drugs matters as much as how many.

The demographic profile has shifted sharply. In 2021, the majority of GLP-1 prescriptions were issued to patients with type 2 diabetes. By 2025, Circana found that 78 percent of users say they are taking the drugs for weight loss, up 41 points from 2021. The RAND data shows use is highest among women aged 50 to 64, while women aged 30 to 49 are more than twice as likely as their male peers to have used a GLP-1. Circana characterizes the typical GLP-1 patient as Gen X, with a household income of over $100,000.

That income profile is not a footnote. Higher-income households are disproportionately likely to purchase premium snacks, specialty retail products, and natural-channel items. When their consumption changes, it shows up fast in the data.

What the Purchase Data Actually Shows

The most rigorous study to date, by Cornell University and Numerator, was published in December 2025 in the Journal of Marketing Research. Researchers tracked grocery and restaurant spending for 2,623 households with at least one GLP-1 user, drawn from Numerator’s 150,000-household consumer panel. They matched these households against surveys that asked when medication began and why.

The headline finding: within six months of starting a GLP-1 medication, households reduce grocery spending by an average of 5.3 percent. Among higher-income households, the drop is over 8 percent. Spending at fast-food restaurants and coffee shops falls by about 8 percent.

The reductions are not spread evenly across the store.

Calorie-dense, ultra-processed foods saw the sharpest declines.

- Spending on savory snacks dropped roughly 10 percent.

- Sweet bakery items, cookies, and sweets declined by similar magnitudes.

The Cornell and Numerator data specifically call out chips, sweet bakery, side dishes, and cookies as showing the largest declines in individual categories, ranging from 6.7 to 11.1 percent.

Numerator’s GLP-1 Trends Hub, launched in October 2025 and built on quarterly surveys of 30,000 consumers, adds another layer. Among GLP-1 users focused on weight loss, packaged bakery, snacks, prepared foods, and beans and grains showed year-over-year buy rate declines of 10 to 20 percent compared to non-users. Users focused specifically on losing 15 or more pounds reduced spending by 10 percent across more than 100 categories in grocery, quick-service restaurants, and tobacco within six months of starting the medication.

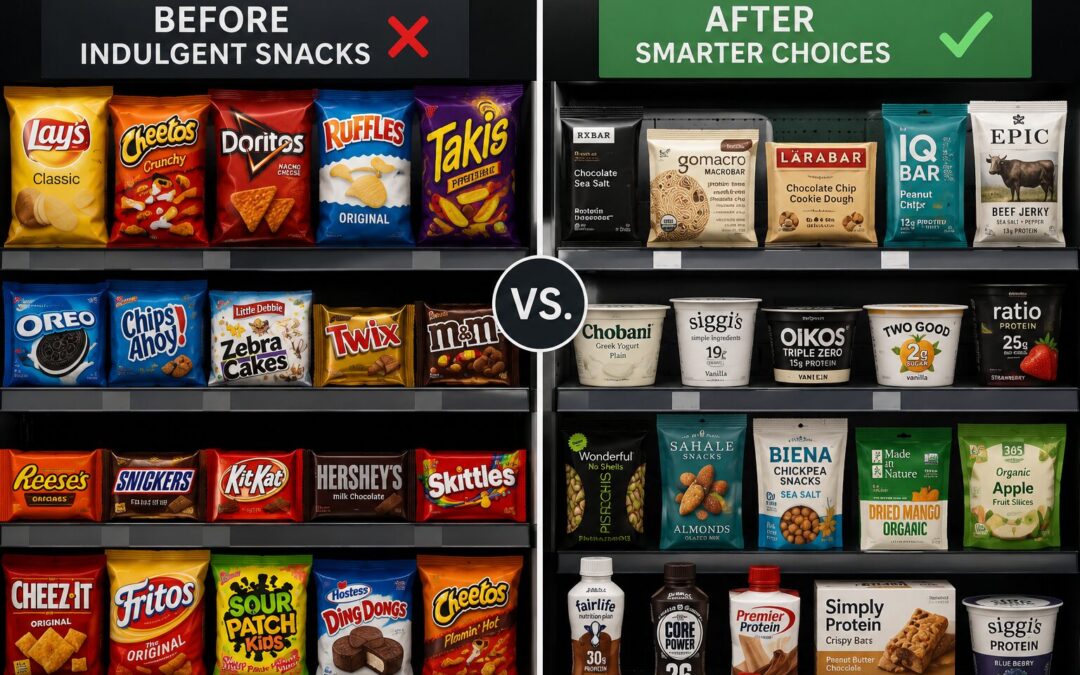

One data point on the other side of the ledger matters here. The Cornell research found statistically significant increases in only a handful of categories: yogurt, fresh fruit, nutrition bars, and meat snacks.

Weight-loss users specifically showed modest increases in fresh produce and yogurt. Protein shakes rose 38 percent among GLP-1 users. Superfoods climbed 58 percent.

The biology drives the basket. GLP-1 drugs suppress appetite and reduce cravings for high-fat, high-sugar foods. Protein becomes increasingly important for preventing muscle loss. Fiber supports digestive health.

Every calorie has to work harder, and users are making choices accordingly.

The Snack Industry Is Not Panicking Yet, but It Should Be Paying Attention

EY-Parthenon has been tracking this closely. Their analysis suggests GLP-1 adoption could put up to a $12 billion dent in snack food market growth and significantly slow the sector’s current 3 to 4 percent annual growth rate.

Survey respondents using GLP-1 drugs for weight loss reported declines in consumption of 40 to 60 percent across snack categories, while specialty and health foods climbed by nearly 50 percent, proteins by 65 percent, and fruits and vegetables by nearly 80 percent.

- General Mills CEO Jeff Harmening told analysts at the Consumer Analyst Group of New York conference that anti-obesity drugs will have a lasting influence on the food market.

The company is reformulating products, launching smaller portion sizes, and adding protein and fiber to existing lines, including Honey Nut Cheerios Protein and Ghost performance nutrition bars.

Nestle launched Vital Pursuit in 2024, its first major U.S. brand in nearly three decades, specifically targeting GLP-1 users with portion-controlled, nutrient-dense frozen meals. Danone rolled out an Oikos yogurt drink in 2025 designed to help GLP-1 users build and retain muscle mass.

Circana’s research adds nuance that matters for brand strategy.

GLP-1 users are still outspending non-users on CPG overall. Their spending shifts away from mass and dollar stores toward club stores and e-commerce.

Convenience stores have an emerging opportunity because the channel is already built around single-serve, on-the-go, and portion-controlled formats. And a meaningful share of users, even when they stop taking the medication, hold onto some of the health-conscious behaviors they adopted while on it.

There is also a rebound dynamic worth watching.

The Cornell research found that about one-third of users stopped taking the medication during the study period. When they did, food spending returned to pre-adoption levels. Indulgent categories like candy and baked goods typically rebound within 3 to 6 months after users stop using them.

- The demand shift is real while users are on the drug. It is not necessarily permanent.

What This Means for Food and Beverage Brands

The short answer is that the brands most at risk are the ones most exposed to calorie-dense, highly processed snack categories with no clear functional story. Chips, cookies, sweet bakery items, and full-sugar beverages are the categories experiencing the steepest declines among GLP-1 households. If your core SKUs are in those aisles, you need to think about this now.

That does not mean the sky is falling on indulgence.

Barclays and Morgan Stanley estimate widespread GLP-1 adoption could lead to a 3 to 5 percent reduction in total calorie consumption across the U.S. That is meaningful, but it is not a wipeout.

Seventy-four percent of Americans say they do not plan to take these medications. The core snack market is not disappearing.

What is changing is the market’s composition.

A growing cohort of health-focused, higher-income consumers is actively shifting their baskets toward protein, fiber, hydration, and portion control. The brands that have already built a story around those attributes are well-positioned. The ones that have not need to decide whether to reformulate, reposition, or find a different lane.

The opportunity is real. SKU proliferation in high-protein, low-sugar, portion-controlled snacks has increased by an estimated 47 percent year over year since 2024. Brands that can credibly claim the protein or fiber positioning, in the right pack size, in the right channel, with a real taste payoff, are moving product.

The harder problem is for mid-market brands without the R&D budgets to reformulate or launch new lines quickly. Those brands need to be honest about where they are exposed, which customers they are losing, and whether a packaging or messaging adjustment can meaningfully help. At the same time, they figure out a longer-term product answer.

One more thing worth saying.

The consumer on a GLP-1 medication is not anti-snack. She is pro-value. Every bite needs to earn its place.

That is an opportunity for brands with a genuine nutrition story, not just a label that says “protein” on the front and has 3 grams of it.

Three Key Takeaways

1. The scale of this shift is no longer speculative. Twelve percent of U.S. adults have now used a GLP-1 drug, and 23 percent of households have at least one user. Cornell and Numerator’s purchase data confirms real, sustained declines of 10 percent or more in savory snacks, sweet bakery, and cookies within six months of adoption. Circana projects GLP-1 households will represent 35 percent of all food and beverage units sold by 2030. This is not a wellness trend you can wait out.

2. Protein, fiber, and portion control are not nice-to-haves anymore. The GLP-1 user is maximizing every calorie. Categories winning in this environment are yogurt, nutrition bars, meat snacks, fresh produce, and high-protein beverages. Brands that can credibly deliver protein, fiber, or portion discipline, and actually taste good doing it, are gaining share. Brands competing purely on indulgence without a functional dimension are losing it.

3. Channel strategy matters as much as product strategy. GLP-1 users are shifting their spending away from mass and dollar stores toward club, e-commerce, and convenience stores. The convenience channel, already built around single-serve and portion-controlled formats, is unusually well-positioned. Distribution in the right channel, paired with the right pack size, is not a detail. For this consumer cohort, it is the difference between being in the consideration set or not.

The snack aisle is not going away. But the consumer walking it is changing. The brands that figure out which job they do for someone eating 30 percent less on purpose, with a very clear sense of what every bite is worth, will be the ones still on the shelf in 2030.

That is not a small ask. But it is the right one.

Connect with Jeff at The Marketing Sage Consultancy. Interested in setting up a call? Use my calendly to schedule a time to talk. The call is free, and we can discuss your brand, marketing needs, and challenges.

Feel free to email me at jeffslater@themarketing sage.com or text 919 720 0995. Thanks for your interest in working with The Marketing Sage Consultancy.